2023 Midyear Economic and Market Outlook Report

2023 looks likely to end with an economic recovery marked by strong regional divergence as nations respond to challenging inflation, tight labour markets and geopolitical turbulence.

Executive summary

The global economy performed well at the start of the year, supported by factors such as falling energy prices, strong consumer balance sheets and the reopening of the Chinese economy. We expect a modest slowdown as we head into the second half of 2023.

Regional divergence is likely as different economies are at varying stages of the business cycle, with China likely to perform well and the US poorly. Annual global inflation rates should continue to fall due to lower energy prices and normalizing supply chains. However, tight labour markets will continue to drive strong wage growth, keeping core measures of inflation elevated until 2024.

Central banks have aggressively tightened monetary policy to restrictive levels in the developed world and have signalled they will soon pause to assess the full impact of these hikes. The way forward remains uncertain as central banks try to strike a delicate balance between fighting inflation and maintaining financial stability.

Equities have performed well up to late May, with US tech stocks benefiting while bank stocks underperformed. Bond markets have rallied due to expectations of lower inflation and an imminent peak in interest rates. Looking ahead, we see opportunities in emerging market equities and certain segments of growth fixed income despite the uncertain macroeconomic environment.

Some key risks remain, including potential contagion from US regional banks (which may lead to a credit contraction in the real economy), a resurgence in inflation and a further deterioration in the geopolitical landscape.

Section 1. Growth - soft, but globally resilient, regionally divergent

Central banks in most parts of the world — with the notable exceptions of China and Japan — have been tightening monetary policy (using both higher interest rates and quantitative tightening) in an attempt to slow economic growth, ease wage growth and reduce inflation. However, the slowdown has only been modest thus far, with unemployment levels at their lowest in decades (Figure 1).

The global economy’s resilience can be attributed to three main factors: a growth boost from China’s reopening, broad strength in consumer balance sheets and an assist from lower energy prices. We expect some of these supporting factors to fade, with a more difficult 12 months ahead for the US, even if China remains strong. However, we don’t expect uniformity across regions as different economies are at varying stages of the business cycle.

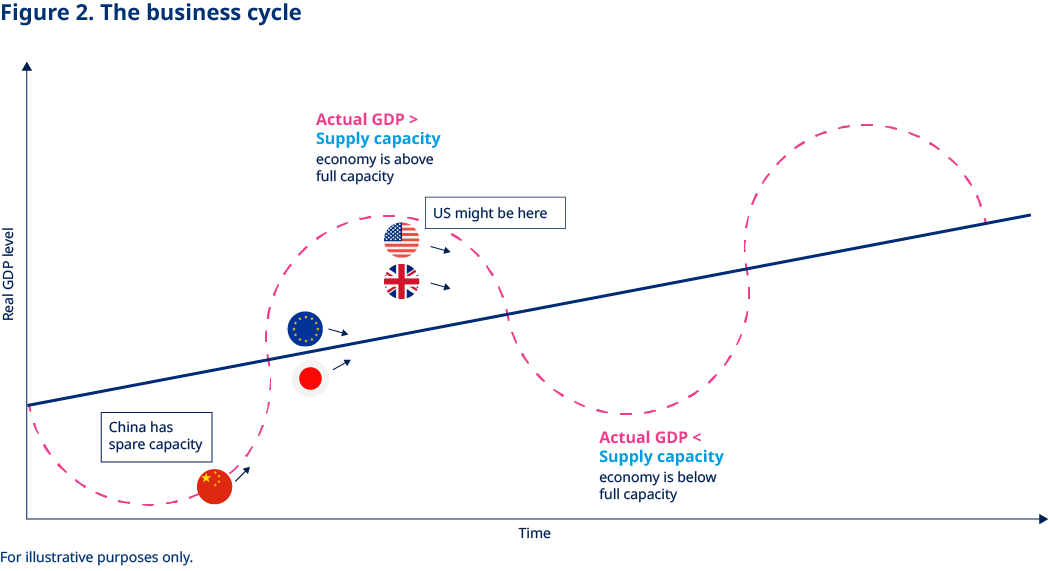

Figure 2 below illustrates a typical business cycle. The blue line depicts an economy’s capacity, which is determined by the amount of labour, capital and total-factor productivity. The red line shows where an economy is, based on consumption, investments, government spending and net trade.

If the red line moves above the blue line, an economy overheats, and tight labour markets lead to higher wages and inflation. In that case, a central bank tightens policy in an attempt to engineer a slowdown and bring the red line back to the blue line.

If the red line is below the blue line, a central bank loosens policy in an attempt to stimulate growth. As shown by the flags on the chart, a number of developed economies have overheated and experienced high inflation, prompting aggressive actions by central banks. Meanwhile, China is in a completely different stage of the business cycle, with plenty of room to grow before overly tight labour markets begin to cause an inflation problem.

We expect the US economy to stall … We maintain our view that a deep recession is unlikely.

We expect the US economy to stall in the second half of 2023 and early 2024 as the assist from lower energy prices fades, consumer savings are used up and banks tighten their lending standards (Figure 3). That said, we maintain our view that a deep recession is unlikely as consumption should be supported by resilient household balance sheets and healthy income growth.

Figure 3 depicts two surveys that measure changes in bank-lending standards to businesses in the US and the eurozone. Above 0% means, on average, banks are tightening lending standards.

The eurozone and the UK appear to have avoided recessions as natural gas prices have fallen sharply, with cost-of-living pressures easing. The extent of overheating in Europe is lower than in the US, so we would expect Europe to fare better in comparison. As shown in Figure 2, the US has overshot its capacity to a greater degree, which means the slowdown to get back to the blue line could be more significant. Because the eurozone hasn’t overshot its capacity by much, the slowdown should be relatively modest.

In the near term, we expect Japan to outperform its developed counterparts since it’s earlier in the cycle and it has the least overheated economy, with the Bank of Japan (BoJ) having taken no major steps to slow it. Meanwhile, there are signs of service inflation in Japan for the first time in decades. Employers and unions have also agreed to perhaps the biggest wage gains since 1993, indicating further upside risks to inflation and implying that easy monetary policy in Japan may not continue forever.

The strength in China will be spurred by a jump in face-to-face economic activity.

The Chinese economy had a difficult 2022, driven by restrictive COVID-19 policies and the aftermath of a major regulatory crackdown in its technology and property sectors that started in 2021. China has done very well in 2023 thus far, boosted by a post-lockdown consumption boom and a recovery in credit creation. It has also been supported by the People’s Bank of China (PBoC) maintaining loose monetary policy. The strength in China will be spurred by a jump in face-to-face economic activity, which will have less impact on the global economy than past recoveries driven by construction and investment.

Nonetheless, there should be wide-ranging economic benefits to China’s trading partners, especially in relation to tourism. More broadly, emerging market (EM) countries didn’t overheat as much as developed market (DM) countries. Their central banks started raising interest rates earlier, and fiscal stimulus wasn’t as excessive as in Western countries, creating a more favourable macro backdrop going forward.

Section 2. Inflation - disinflation continues but at a slower pace

In Japan, inflation is the highest it has been in several decades.

Headline inflation rates are falling … driven by lower energy prices and normalizing supply chains.

In Japan, inflation is the highest it has been in several decades, with headline inflation at 3.5% and core at 4.1%. Here, it’s especially notable as it’s happening alongside increases in both wage growth and inflation expectations, raising the probability that Japan has at last exited its long period of deflation. If confirmed, the BoJ would need to begin unwinding its ultra-loose monetary policy.

In China, inflation is very low, with the headline reading at 0.1% and core at 0.7%; unemployment is higher than normal, keeping wage growth low. Inflation is broadly elevated in EMs but not as high as in DMs (compared to average inflation rates).

Looking ahead, we expect inflation to continue to fall but recognize that reducing inflation from approximately 5% to 2% is likely to be a harder and longer process than the jump from 8% to 5%. The key reason for this is that labour markets need to weaken materially for wage growth to fall, and wage growth adjusts slowly and at a lag to economic changes. For inflation to hit 2%, wage growth needs to be close to 3%–4%, with the difference being productivity growth.

As it stands in the US, wage growth is closer to 5% — a rate consistent with consumer price inflation of 3%–4%. We observe similar dynamics in the eurozone, the UK and Japan. Tighter monetary policy should eventually lead to higher unemployment and lower wage growth, but this will take time.

Section 3. Central banks - pause and assess

Central banks have increased interest rates significantly to bring them above the neutral rate. For reference, the neutral rate of interest is a theoretical policy rate that neither stimulates nor slows economic growth.

Since the start of 2022, the US Federal Reserve (“the Fed”) has raised interest rates by 5.0% (from 0.25% to 5.25%) in one of the most aggressive tightening cycles ever. We expect the Fed to hold interest rates at the current level for the rest of the year. Once it has a clear line of sight for core inflation returning to 2.0%, it may begin normalizing policy. In practice, this is likely to mean rate cuts in the first half of 2024. The risk of the Fed having to raise interest rates all the way to 6.0% is much lower than it was at the start of 2023 because of ongoing US regional bank stress and the subsequent tightening of bank lending standards.

The European Central Bank (ECB) raised interest rates by 3.75% (from 0% to 3.75%). We expect it to increase interest rates above 4% in 2023 followed by a pause for the remainder of the year to ensure inflationary pressures from an overheated labour market subside.

The BOE has the most difficult job of all, with inflation still quite elevated (both core and headline) despite raising rates by nearly 4.5%.

The Bank of England (BOE) has the most difficult job of all, with inflation still quite elevated (both core and headline) despite raising rates by nearly 4.5% (from 0.1% to 4.5%). We expect it to increase interest rates above 5% in 2023 and then a pause. Interest rate cuts are only warranted if the UK economy takes a sharp leg down and inflation decelerates at both core and headline levels.

The BoJ has so far resisted pressure to materially tighten monetary policy, which we believe is an increasingly difficult stance to maintain. A resilient economy, elevated headline and core inflation, rising wages, and an increase in short and medium-term inflation expectations all point to the need to tighten monetary policy. We expect the BoJ to relax its yield-curve-control policy in the near term and possibly raise interest rates in 2024 or 2025.

Unlike most central banks, the PBoC continues to ease policy in an effort to stimulate economic activity. We expect that to continue for the rest of the year. Ex-China EM central banks tightened policy early to fight inflation and defend depreciating currencies. We expect them to move toward a less aggressive policy stance and bring interest rates down to neutral levels.

Section 4. Markets - clip the coupon on growth fixed income in times of uncertainty

Figure 7 shows the difference between yields on global corporate (high-yield and investment-grade) bonds and government bonds of the same maturity.

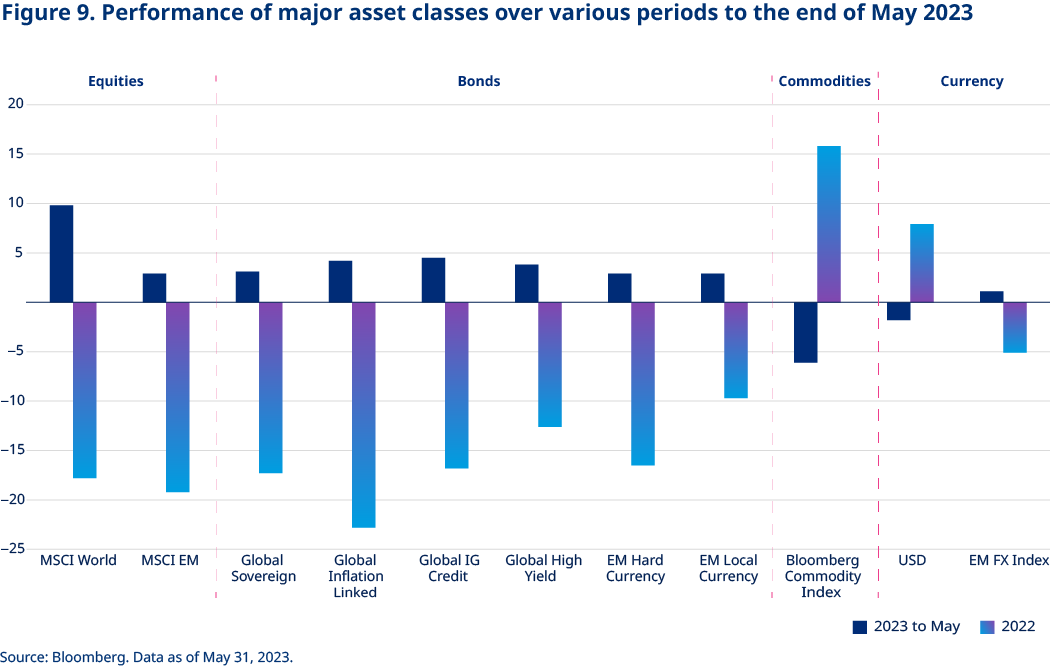

So far, 2023 has been a positive year for equities despite the uncertainties surrounding US regional banks, the Fed, high inflation and fears of recession. Global equities have risen 9.4% (in USD terms) as of May 15, 2023. European equities have been particularly strong this year, driven by more attractive valuations, strong demand from Chinese consumers and a material rollover in natural gas prices. EM equities underperformed despite a strong economic backdrop driven by accelerating Chinese growth.

Bonds have rallied in 2023 given expectations of lower inflation, slower growth and a pause in central bank interest rate hikes. US regional bank distress has led to a highly volatile (particularly in short-term maturities) repricing of peak Fed interest rate expectations, driving other bond market pricing too.

Within equities, we see opportunities in EMs on the back of cheap valuations and strong earnings impetus.

Credit spreads haven’t moved much year-to-date (Figure 7). Local-currency EM debt posted 3.4% (in USD terms), whereas hard-currency EM debt returned 1.8% (in USD terms), as at 31 May 2023. In currency markets, we’ve seen a softer US dollar, stronger euro and sterling, weaker yen, and stronger EM currencies.

We don't hold high-conviction views on equities as an asset class. Although valuations remain unimpressive (Figure 6) and earnings expectations somewhat too optimistic, we find market positioning to be overly bearish, which balances our overall view to neutral. Within equities, we see opportunities in EMs on the back of cheap valuations and strong earnings impetus provided by the rebound in China.

We believe allocations to certain segments of growth fixed income remain attractive.

We believe allocations to certain segments of growth fixed income remain attractive and can potentially help create a cushion of income in a portfolio, making it more resilient in times of high macro uncertainty. Both investment-grade and high-yield credit spreads appear to remain at reasonably attractive levels and may offer sufficient compensation for taking on default risk. We think EM local-currency debt is attractive, driven by cheap currencies and attractive bond yields.

We expect the US dollar to depreciate against DM and EM currencies. Softer-than-elsewhere economic growth, unique political challenges, twin deficits (trade and fiscal) and expensive valuations should set up the global reserve currency for multiyear weakness. The yen should appreciate against the US dollar as the BoJ moves toward tightening its monetary policy while the Fed remains largely on hold. We’re constructive on both the euro and sterling versus the US dollar as we expect the ECB to be relatively more hawkish than the Fed and the eurozone economy relatively stronger than the US. We’re broadly constructive on EM currencies driven by attractive valuations.

Section 5. Key risks - banks, inflation and geopolitics

When asked what keeps us awake at night, we would note the risks below.

Contagion from the US regional banking crisis (Figure 8): US regional bank distress still has the potential to spill over into larger banks and to banks outside the US, causing a broader credit crunch. However, we believe this scenario is unlikely due to the significantly improved capitalization of banks, robust bank profitability and the determination of policymakers to ensure the stability of the financial system, which is closely aligned with a stable banking sector.

Persistent inflation: Although we expect headline inflation to decrease significantly in the near term, it’s less clear if and when core inflation will fall sustainably to central banks’ 2% targets. A delay could force central banks to keep interest rates high for some time or even raise them again after a pause.

Geopolitics: A further deterioration in US–China relations may lead to additional trade restrictions and potential military confrontations, both direct and indirect, between the two global superpowers. A further escalation of the ongoing war in Ukraine remains a risk, with far-reaching impact politically, economically and, more importantly, in terms of the human cost.

Section 6. Portfolio positioning

Although uncertainties remain in the macro outlook, we prefer growth fixed income assets (high yield, and emerging market debt) to defensive fixed income assets and cash.

We remain neutral on equities as, on balance, valuations look fair. Although further declines in inflation should support equities, we think corporate profit growth won’t impress in the developed world in 2023. We remain overweight on emerging equities as we expect the recovery in China to generate strong economic and corporate profit growth. A generally weak US dollar should also support emerging markets.

We expect the US dollar to continue depreciating against DM and EM currencies.

Appendix