Defined Contribution Plan Fee Practices

Effective fee management is a critical component in maximizing retirement readiness and minimizing fiduciary risk.

Participants in defined contribution (DC) plans rely heavily on plan sponsors and fiduciaries to design and monitor a cost-effective program that helps them to achieve a secure retirement. In addition to expecting top-tier customer service from DC plan vendors and access to high-performing, low-cost institutional investment vehicles, participants also want to ensure that the growth of their account balances is not subject to “hidden” or uncompetitive fees.

Against this backdrop, DC plan fees are the target of intense scrutiny from legislators, regulators and litigators, as lawsuits continue to grab headlines. The Department of Labor’s (DOL’s) existing service-provider and participant disclosure requirements signal its continued intention to enforce the requirement that the compensation paid for all service relationships funded by ERISA plan assets be “reasonable.”

Effective fee management is a critical component in maximizing retirement readiness and minimizing fiduciary risk. As little as 20 basis points (0.2%) in excess fees could reduce the payout of retirement benefits by as much as $300,000 over an employee’s lifetime.1

Mercer's Fiduciary Best Practices2

Based on DOL guidelines, case law and extensive marketplace experience, Mercer has established the following robust practices to assist committee members in satisfying their fiduciary requirements:

-

Price administrative fees on a per-participant basis.Negotiate a fixed-rate recordkeeping fee – based on the number of participants with account balances in the plan – that is independent of the investment structure (referred to as an “open investment architecture” model) or other unrelated offerings provided by the recordkeeper (e.g. HSA administration). This approach, unlike an “asset-based” or “bundled” model, provides fee transparency and affords fiduciaries a sound basis for documenting the “reasonableness” of recordkeeping fees. Conversely, utilizing a pricing model that is dependent on the value of plan assets arbitrarily “builds in” fee increases that are not linked to the level or quality of the recordkeeper’s services.

-

Benchmark and negotiate recordkeeping and investment fees separately.

Due to some recordkeepers’ preference for bundling DC plan services, fees, and investments, some plan sponsors may view fees from a total cost perspective.

In our view, a prudent fiduciary should evaluate and monitor investment fees and recordkeeping fees separately. In cases where the recordkeeper offers proprietary asset management, the plan sponsor should maintain fiduciary flexibility by negotiating a contractual provision that allows the continuance of more favorable recordkeeping fees in the event that some or all of the recordkeeper’s funds are removed from the plan’s lineup for underperformance.

-

Benchmark and negotiate investment fees regularly, considering both fund vehicle and asset size.

Plan sponsors can mitigate fiduciary risk by selecting the lowest expense ratio and/or lowest net cost vehicle for each investment option regardless of whether revenue sharing is reduced or eliminated. Less expensive alternatives to mutual funds, such as collective investment trusts and separately managed accounts, are increasingly available in the marketplace. These mutual fund alternatives should be evaluated and used when they offer lower overall fees, barring any sponsor-specific concerns or constraints. To potentially minimize investment costs, plan sponsors must be proactive and monitor investment fees as plan assets grow and markets evolve. Investment managers often do not inform clients of eligibility for new and/or lower-cost investment vehicles as they become available.

Furthermore, for employers sponsoring multiple plans offering the same funds, investment managers typically aggregate assets to determine eligibility for lower-cost investment vehicles. To help ensure that this aggregation occurs, communication from the plan sponsor or service provider is often required.

-

Benchmark and negotiate recordkeeping and trustee fees at least every three years.Comparing a plan’s recordkeeping and trustee fees to the fees of other plans based on survey data or publicly available information does not provide a fiduciary safe harbor for monitoring the reasonableness of fees. DC plan fees vary based on each plan’s complexity, size, and required level of services. By conducting a fee benchmarking study every three years, using market data specific to your plan’s service requirements rather than broad survey information, fiduciaries can document that the plan’s fees are market competitive or determine the need for additional action (e.g., negotiations with current recordkeeper or conducting a vendor search).

-

Negotiate vendor contracts to help ensure that service standards and liability provisions are in the best interest of plan participants and beneficiaries.

The contract should clearly identify vendor responsibilities and hold vendors fully responsible for any contractual breach caused by their negligence. Service standards should be meaningful to the plan sponsor, reflective of services delivered to the sponsor specifically and measurable by the vendor with fees at risk for failure to meet service standards. For example, vendors could be held accountable for the improvement of a plan’s aggregate retirement readiness.

Furthermore, with the increased risk of cyberattacks on the US financial industry and the Department of Labor’s Cybersecurity Program Best Practices, vendor contracts should be updated regularly to address current data security policies and exposures in the event of a data breach.

-

Monitor actual fees paid against contractual requirements.Provider disclosure requirements under ERISA Section 408(b)(2) are designed to ensure that sponsors are aware of their fee arrangements. It is incumbent upon the sponsor to ensure that actual charges align with contractual provisions and disclosures.

-

Review services annually to identify opportunities to reduce administrative costs.

An annual review of opportunities to reduce the overall cost of administration often leads to fee reductions. Areas to consider include:

- Administrative processes that are inefficient or outdated.

- Underutilized services or plan provisions that can be eliminated.

- Plan provisions that can be simplified or streamlined.

- Participant notices and documents that can be delivered electronically to reduce mailing costs as well as the environmental impact.

- Internal processes that could be outsourced.

- Internal controls to help reduce errors.

- Strategies to promote automation and self-service among participants.

- Consolidation of legacy plan accounts to reduce plan complexity.

- Elimination of legacy communication campaigns that have no discernible impact on participation, asset allocation, or retirement readiness.

-

Monitor third-party revenue sharing arrangements.

Request information about revenues that the recordkeeper may receive from third parties as a result of participants utilizing certain services.

For example, if a plan offers investment advice or managed account services to its participants, is the revenue generated from this program disclosed to the plan sponsor and treated in accordance with the vendor contract?

Further, with the rise in recordkeepers partnering with third parties to offer financial wellness solutions to plan participants, the third parties should fully disclose their fees and any revenue sharing arrangements with the recordkeeper.

Importance of fee allocation

In addition to ensuring that DC plan fees are reasonable with respect to the services provided, fiduciaries are also responsible for the fair and appropriate allocation of fees that are paid directly or indirectly by participants.

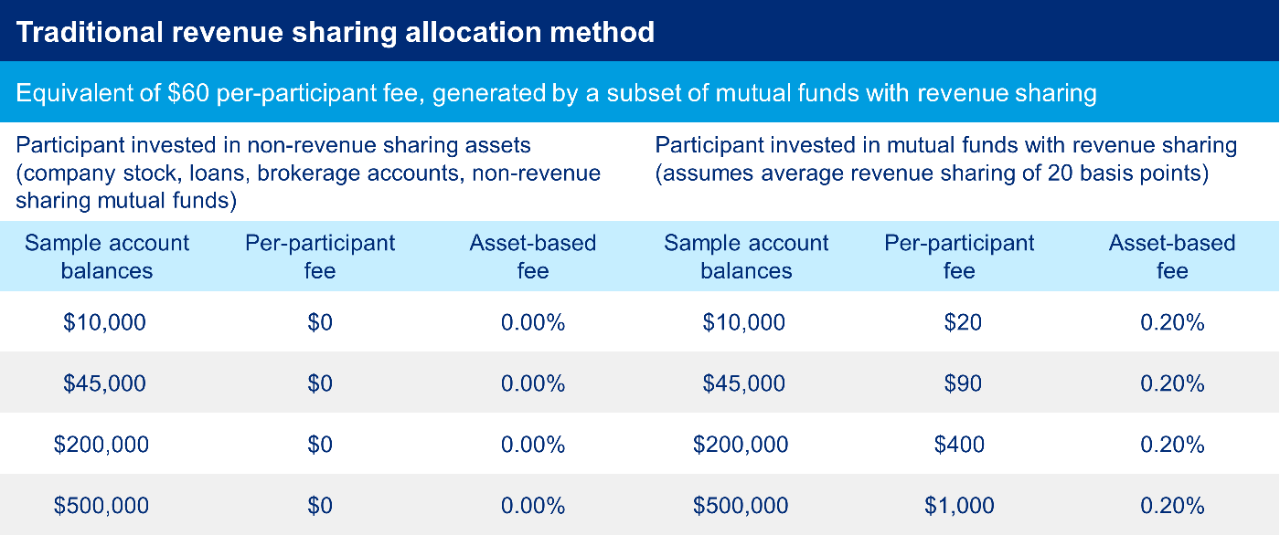

Some plan sponsors may be unaware that they have inadvertently selected an allocation method by using revenue sharing from the plan’s investment options to offset recordkeeping fees. Since the rate of revenue sharing typically varies across investment options, some participants disproportionately bear the recordkeeping costs of the plan on behalf of participants who invest in low or non-revenue sharing options. The appropriateness of revenue sharing has been targeted in DC plan fee litigation using the argument that the fee allocation does not bear a direct relationship to the services being provided.

For the reasons described above, we believe it is important to consider eliminating revenue sharing to the extent possible. If it is not feasible or appropriate to entirely eliminate revenue sharing, plan sponsors can consider crediting revenue sharing to those participants invested in the fund options that generate revenue sharing. Administrative fees can then be allocated through a hard-dollar fee that is more transparent to participants.

Generally, administrative fees can be allocated to participant accounts on a per-participant basis, based on asset levels, or in combination. As mentioned earlier, a per-participant fee is considered best practice by Mercer and is in line with how recordkeeping costs are generated.

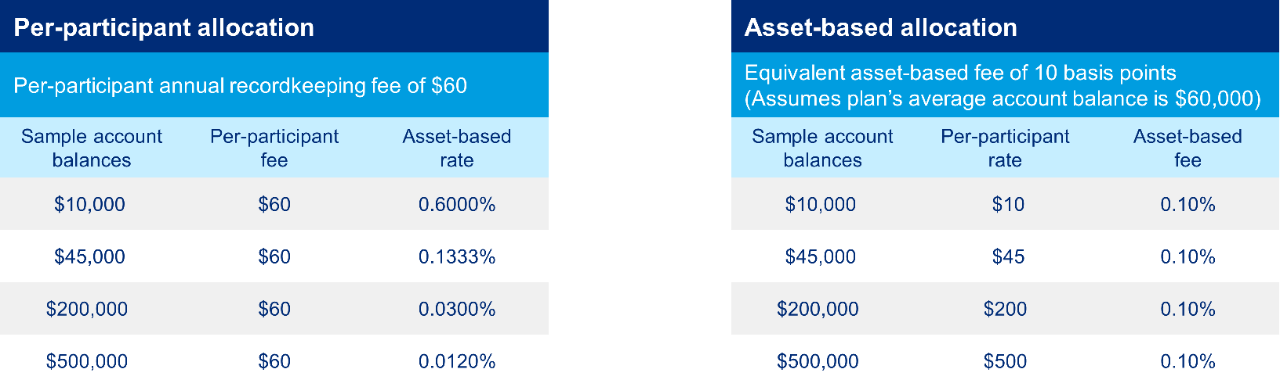

Recordkeeping fee allocation methodologies’ impact on individual participants

The tables below compare the annual cost to individual participants of a per-participant fee to the cost under two different asset-based methods.

The per-participant approach, while the most equitable, creates a higher-percentage allocation to small-balance accounts. Sponsors with high turnover or significant low-paid populations may fear that this result will negatively affect participation among this group. One way to mitigate this impact is by waiving the fee for balances under a set dollar threshold or for new accounts (plan sponsor would absorb those fees as an employment benefit) — for example, for accounts under $5,000 or held by participants during their initial year of employment. This strategy may be helpful in plans that have an auto-enrollment feature.

When switching from revenue sharing to per-participant hard-dollar recordkeeping fees, plan sponsors often worry about adverse responses from participants. Although making this change may present a communication challenge, Mercer’s experience has been that participants adjust quickly to seeing a fee on their quarterly statements and the level of reaction is typically negligible. For those participants who do take notice, there is an opportunity for education around the reason for plan fees and the efforts of the plan sponsor to manage fees. Further, when fee structure changes are paired with changes to lower-cost investments without revenue sharing, this results in an overall reduction in plan fees and expenses, on average, for most plan participants.

When services or investment vehicles span more than one plan (including non-qualified plans), care must be taken that the allocation of fees and crediting of any income between plans are appropriate. The methodology and rationale for allocation between plans should be clearly documented.

Monitoring transaction fees

In addition to basic recordkeeping fees, recordkeepers often charge for participant-initiated transactions and services such as loans, withdrawals, domestic relations orders, brokerage accounts and professionally managed accounts. Mercer believes it is appropriate to have participants bear the cost for services they request, rather than spreading those costs across the general population.

Transaction fees may also play a part in discouraging loan and withdrawal activity that contributes to plan leakage. Plan sponsors need to consider whether transaction or use-based fees should apply in other areas, such as administration of company stock accounts and Roth in-plan conversion — if such features are offered by the plan.

Keep in mind, however, that fee compression in the recordkeeping industry has led to, in some cases, a sharp increase in certain transaction fees. It makes sense to review transaction-based fees as part of the ongoing fee review and consider these fees in any negotiations to reduce the overall cost structure. Sponsors must consider whether negotiated fee reductions should be applied to overall administrative costs, transaction fees or both.

Document, document, document

Most plan fee litigation hinges on procedure rather than outcome. It is critically important that plan fiduciaries explicitly address their responsibilities around DC plan fees, document their efforts through committee minutes or other official records, such as a fee policy statement, and require recordkeepers and other plan service providers to proactively address fees.

A fee policy statement sets out activities and procedures designed to promote oversight and fee management, including:

- Delegation of responsibilities regarding fees and expenses.

- Identification and documentation of fees charged to plan assets or paid by the plan sponsor.

- Procedures for approving expenses and fees to be charged to plan assets.

- Documentation of efforts to help ensure that plan fees are reasonable in light of the services provided, including ongoing monitoring of fees and expenses.

- Procedures for fulfilling annual reporting and disclosure requirements, including government filings and participant disclosures.

Steps for plan fiduciaries to consider

As the fiduciary landscape continues to evolve, plan sponsors should take steps to help ensure that they fulfill their duties to participants while minimizing their own fiduciary risk.

- Document your review of disclosures from covered service providers to ensure that all required disclosures have been received.

- Appropriately benchmark plan administrative fees and investment fees, paying particular attention to whether there are less costly share classes or vehicles available for the same strategy.

- Document the evidence relied on in concluding that plan service relationships and fees are “reasonable.”

- Ensure that fee disclosure requirements are being met — both to participants and to the DOL via Form 5500, Schedule C.

- Review the allocation methodology for all fees charged to participants or to plan assets.

- Establish an ongoing fee management structure and policy in a Fee Policy Statement.

The increased demands placed on DC plans, combined with the intense focus on fees, ultimately call for greater attention to fee management, allocation and documentation. Effective fee management may improve retirement outcomes for plan participants while seeking/pursuing risk mitigation and enhanced plan performance.

1 Assumes employee starts career at age 25, retires at age 65, starting pay of $40,000, annual pay increases of 2.5%, employee plus employer annual contributions of 10% of pay, investment return of 7% pre-retirement and 5% post-retirement, and initial annual retirement withdrawal of 4% of balance increased by 2.5% each year for inflation. Mercer calculations as of 5/31/2024. Analysis performed on 5/31/2024. Shown for illustrative purposes only.

2 The information contained in this document is provided for informational and educational purposes only. The opinions expressed are subject to change without notice. The material was prepared without regard to specific objectives, financial situation or needs of any investor. Reliance upon information in this document is at the sole risk and discretion of the reader. Please note that “Mercer’s best practices” were developed based on general principles and without reference to any specific plan sponsor or employer. The circumstances of any given plan sponsor will be unique, and, as with any fiduciary decision, these sponsor-specific circumstances should be taken into account in determining whether and/or how to implement these practices. Accordingly, individually considered plan sponsors’ decisions on these topics may not align with these practices.