Financial concerns remain top of mind for American workers

American workers are changing their spending and saving patterns as personal debt levels rise.

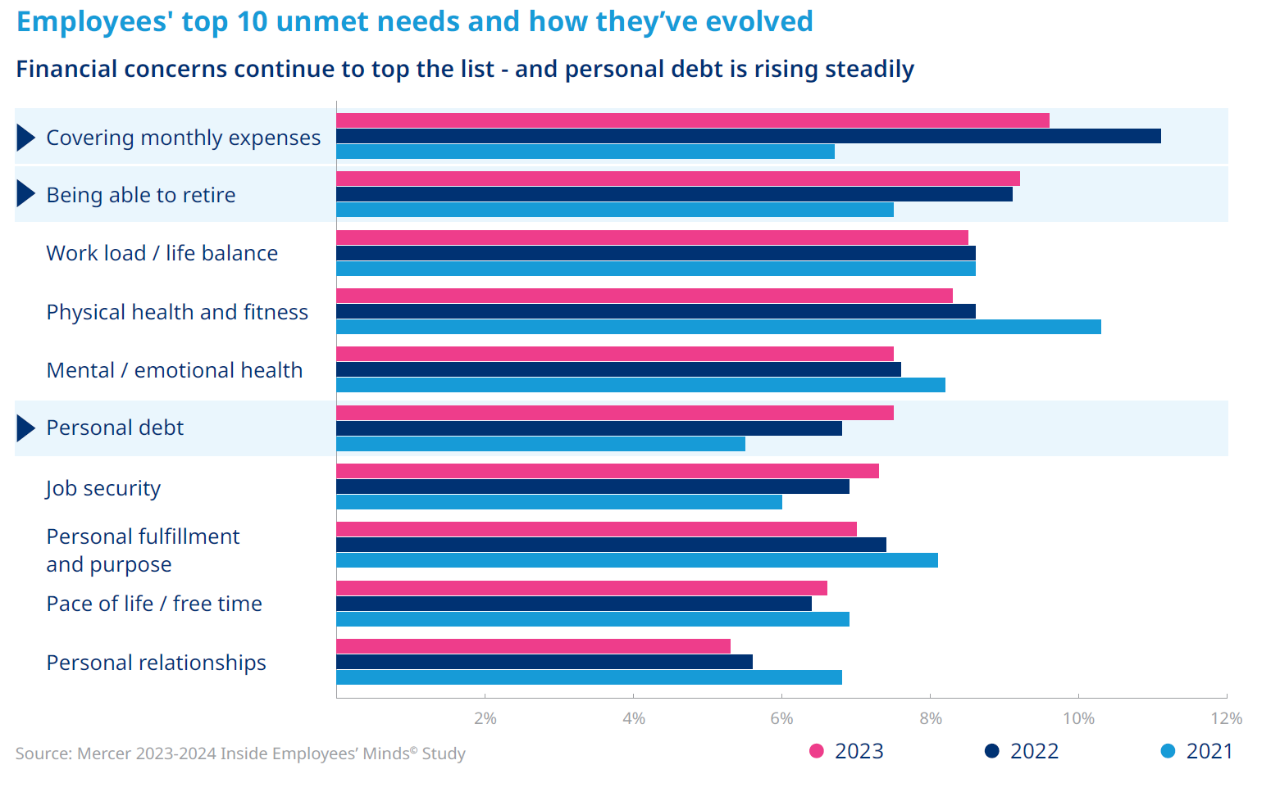

In light of persistently high inflation and market volatility, financial concerns remain top of mind for American workers. According to Mercer’s 2023-2024 Inside Employees’ Minds© study, employees are most concerned about covering monthly expenses, being able to retire and, for lower-income workers, rising personal debt levels. It’s a big change from our 2021 survey, which showed that employees were most apprehensive about their physical health and work/life balance.

Financial stress can affect employees’ work performance and lead to turnover. Fully 39% of employers rate their employees' financial well-being as a high concern in 2023, up from 29% last year[1]. That said, defined contribution (DC) plan sponsors are well positioned to help their employees face their financial futures with confidence by making strategic enhancements to investment menus.

1 EBRI 2023 Financial Wellbeing Employer Survey, September 2023

Financial stress continues to rise

Despite cooling inflation, financial stress has only materially declined for highest-income workers, i.e., those making more than $100,000 per year. The study shows that many workers are reducing spending and savings to help alleviate the pressures they’re feeling from headline inflation. In addition, younger workers are generally more likely to worry about covering everyday expenses, credit card debt and healthcare costs than older workers, who tend to be more focused on long-term financial goals. While those over the age of 45 are tapping into savings at a lower rate than employees under 45, they are more vulnerable to a savings shortfall given their closer time horizon to retirement.

“Among young employees, LGBTQ+, Black women, people with disabilities and the lowest earners, mental health concerns were more pronounced.”

Workload and life balance

A third or more of all employees say they feel work is "exhausting, chaotic, overwhelming or frustrating" on a typical day. Among young employees, LGBTQ+, Black women, people with disabilities and the lowest earners, mental health concerns were more pronounced. When employees were asked what type of support would most benefit their mental health and prevent burnout at work, they pointed to changes in work practices: More time off, reduced workloads, better resources and more flexibility. Employers have made progress over the past few years in increasing access to mental health care providers, and many employees value this type of support. Nearly a fifth cited “enhanced EAP services” as one of the top three benefits or action that would be of help. While it’s clearly important to help employees manage mental health issues and burnout when they arise, survey results suggest that changing work practices might help prevent them. Employers should also be mindful of how financial stressors can contribute to the strains on mental health.

DC plan strategies for supporting employees

As employees struggle with managing rising debt levels or tap into their savings to help meet today’s needs, their retirement plan assets need to work harder. Employees nearing retirement are more vulnerable to market volatility because they have less time for their investments to recover before they need to start withdrawing, and younger workers are missing out on the value of compounding. Furthermore, uncertainty about how to turn savings into income during retirement could lead to workforce management issues in the future.

But DC plan sponsors can help. Consider these strategies:

Learn more about your employees’ most pressing needs and how you can help meet them by reading the full 2023-2024 Inside Employees’ Minds© study.

About Inside Employees' Minds

This study includes 4,505 full-time employees in the United States, working for organizations with more than 250 employees. The study was conducted during the second quarter of 2023. The report also includes actionable advice for employers to help address unmet needs in their workforce. Learn more here.

Click here for important notices.